IBM

IBM fellow Jon

Casey examined “System Scaling Technologies and Opportunities for Future IT

Workloads and Systems” He notes that silicon performance advancement is becoming

more challenging as scaling is becoming more costly and that we need to look

beyond CMOS for cost effective technology solutions. He proposes integrated

co-development of Silicon and packaging solutions to achieve new technologies

with superior cost/performance metrics.

Volumetric scaling will be critical to future

performance enablement

– Tightly

coupled modules and components– 3D stacking and interposer integration

Casey

examined the current state of interposer substrates and showed the following

comparison:

Linx

Linx consultants

looked at “Chemicals and Materials in Semiconductor Devices” . IFTLE notes that

an examination of materials suppliers shows that while chip production is

moving out of Japan due to cost, Japan still has quite a few of the major

materials suppliers on its shores.

Linx lists 3DIC

among the major 5 challenges for the IC industry in the future.

Like many

other prognosticators, Linx points to the cost of 450mm fabs as the main cause

of the ever shrinking customer base .

IMEC

An Steegen,

Sr VP, IMEC examined “Scaling Beyond 10nm”. She offered the following roadmaps

for 3D applications and TSV dimensions.

and the following CoO Analysis for their

3D process flow:

IHS

IHS examined

semiconductors in the electronics value chain.

An unexpected piece of data is that consumers are spending more on

hardware (HW) than content i.e.:

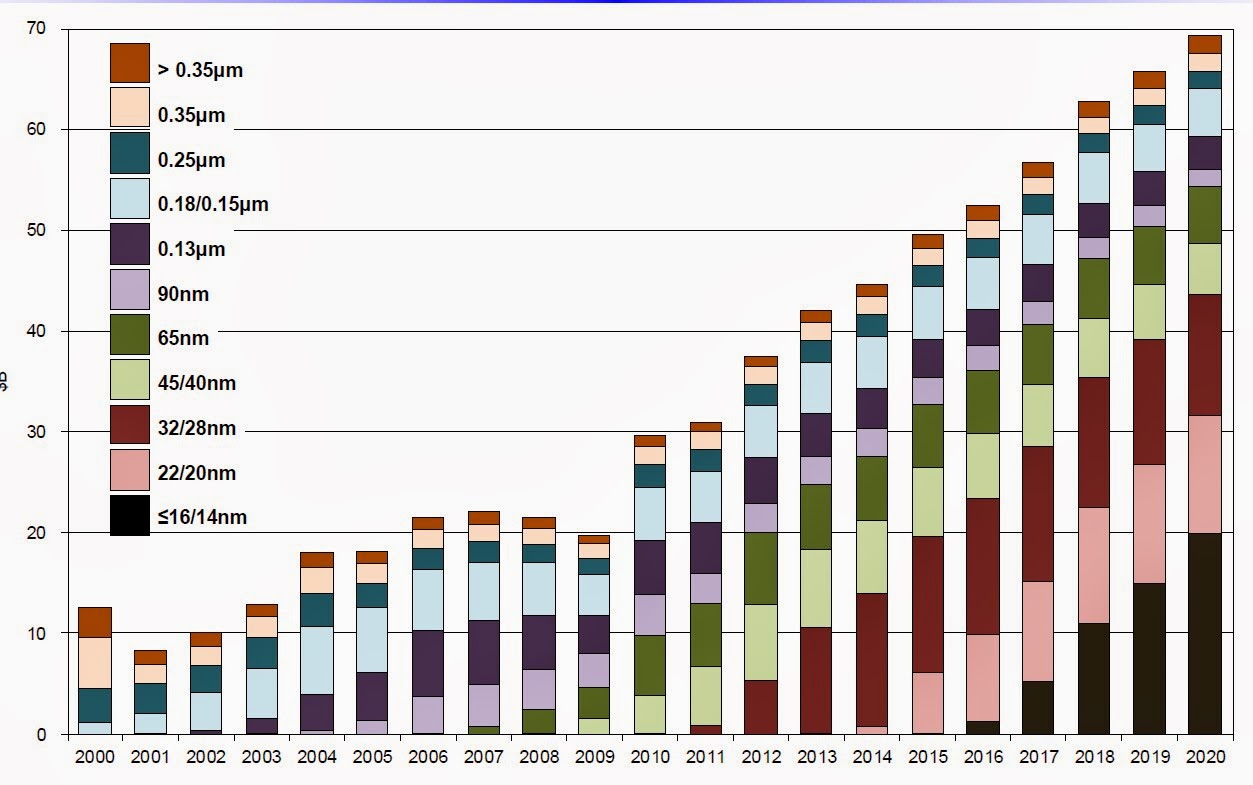

IBS

Our friends

at Int Business Strategies (IBS) who in the past have contributed significant

data to IFTLE arguments that 3DIC makes economic sense in light of the other

scaling options, addressed They indicated that growth in 2013 was mainly due to

an increase on memory pricing. They expect Capex decreases in 2014 (small

decline) and 2015 (large decline).

While there

is uncertainty in the timing for scaleup of 20 and 16 nodes, by 2020 they

expect greater than ½ semi sales will come from 32nm and below.

They also

conclude that low power and low cost will dominate the application space for

32nm or less devices.

They continue

to predict that cost/gate will no longer be a cost driver.

For all the latest on 3DIC and

advanced packaging stay linked to IFTLE……………

No comments:

Post a Comment